Independent Thinking®

Weighing Policy, Inflation and Rates in the Trump Administration

April 21, 2017

Well-researched, investment-grade municipal and corporate bonds remain an important part of a balanced portfolio, even if market expectations of “Trumpinflation” come to pass. Bonds, unlike many other asset classes, are uncorrelated to equities and, in our view, should continue to generate positive returns, net of taxes, inflation and fees over the long term.

It’s important to note that a president can only directly control fiscal policy; the independent Federal Reserve controls monetary policy, which is the more powerful mechanism to regulate inflation through interest rates. While the President has opportunities to appoint the Fed board members, including the chairperson in January 2018, the Fed is likely to continue on its current course of slowly raising interest rates. Fiscal policy can be powerful, however, and can impact both inflation, and state and local government finances.

INFRASTRUCTURE AND DEFENSE SPENDING

Funding for infrastructure and defense, as promised by President Trump, could come from some combination of increased national debt levels, cuts in other spending programs, public-private partnerships, or one-time gains on revenues from taxes on corporate foreign earnings. To the extent that additional spending is funded with new debt, it would increase the level of new money in the system, which theoretically would push prices up. This infusion of money would affect inflation only temporarily, however, unless the infrastructure spending was put to use on capital projects that had a longer-term impact on economic productivity. For example, a bridge that reduces the average commute in a metropolitan area would drive lasting productivity gains, while repaving a road that was already in good shape would not have a similar multiplier, or longer-term effect.

TAX REFORM

The president and Congress have proposed a number of different tax policies, most of which would reduce the rate of taxes for corporations and individuals, and would broaden the tax base by eliminating loopholes. Most economists agree that these measures would be positive for growth and also cause some inflationary pressures. But as always, the devil is in the details. Some of the specific tax policies proposed lack economic consensus regarding their impact on growth and inflation. For instance, the Border Adjustment Tax, which would place a 20% tax on all imports and a tax subsidy on all exports, is largely seen as inflationary, as consumers would likely incur much of that price increase. There is no consensus on whether this policy would spark meaningful economic growth. At the other end of the spectrum, the proposal to disallow corporations to deduct interest costs would disincentivize companies from taking on high debt loads, potentially reducing corporate leverage, which is deflationary.

PROTECTIONIST TRADE POLICY

Trade policy was an important plank in President Trump’s campaign, and he has continued strong protectionist rhetoric since the inauguration. While it remains unclear what, if any, protectionist trade policies will be implemented, we would stress that policies that result in reduction of global trade, such as tariffs and quotas, have a generally negative effect on global growth and increase inflation. This assumes domestic production is more expensive than the goods being imported, as is usually the case in the United States. Consumers are then left purchasing higher priced foreign goods (due to tariffs), or a reduced supply of foreign goods (due to quotas), forcing them to purchase higher cost domestic goods.

DEREGULATION

President Trump and his advisors have focused their deregulation rhetoric on the financial services, energy and healthcare industries, aiming to lower the cost of doing business and, in turn, spur growth. The likely effect on inflation is more mixed. For example, energy deregulation would likely result in increased energy supply, which would be deflationary, while financial services deregulation could result in an increase in lending by community banks, which would be inflationary.

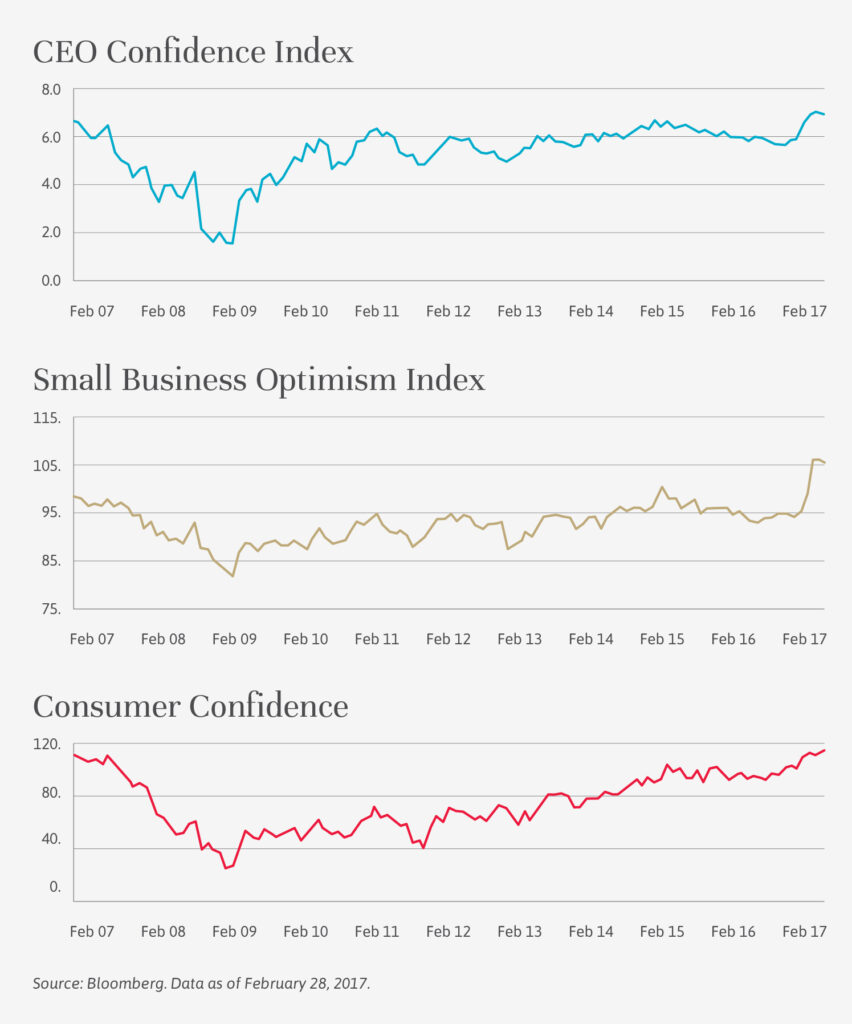

ANIMAL SPIRITS

Pro-growth policies can have a significant impact on inflation, as well as on economic and corporate growth. The more confidence people have in future growth, the more they may invest in the economy, creating the potential for a self-fulfilling virtuous cycle. As the chart on page 8 indicates, there are some early economic indicators that animal spirits have heightened since November; we have seen spikes in confidence levels among consumers, small businesses and CEOs.

While not every Trump policy will be inflationary, the aggregate is likely to have at least some inflationary impact. But there are other factors, both long and short term, that could mitigate these effects. The Federal Reserve has begun its interest rate hiking cycle, and its officials have said that they expect to increase rates another two to three times in 2017. Higher interest rates could cool inflation by increasing the cost of debt and slowing both consumer and corporate borrowing, potentially curtailing growth in key sectors of the economy, such as housing. The strong U.S. dollar, which has increased against most other currencies since the election, with many market participants anticipating further strength, is also potentially disinflationary or deflationary. (See the chart on page 8.) A strong dollar can decrease earnings of U.S.-based multinational companies, hurt U.S. exports and reduce commodity prices, and also hurt emerging market economies.

Longer term, aging demographics, technological advancements that reduce the need for human labor, and unsustainably high levels of national debt relative to GDP are all deflationary forces that could mitigate the effect of Trumpinflation and stem increases in interest rates.

For bondholders, the primary concerns are twofold: Policies could have an adverse impact on credit by negatively affecting state and local finances or an adverse impact on interest rates via rising inflation or growth. Municipal bond and U.S. government bond interest rates have already made a significant move higher, with the 10-year Treasury rising to 2.25% (and as high as 2.63% in mid-March) from 1.85% prior to the election. If inflation expectations continue to rise and the Fed continues to hike interest rates in 2017, rates may rise and bond prices will fall.

Even if we make the somewhat draconian assumption that interest rates continue to rise from today’s level to 5% for a 10-year Treasury five years from now, a hypothetical portfolio of 4.5-year duration bonds would still manage to eke out a small positive gain of around 1% net of taxes each year – below inflation expectations, but still positive.

So why hold bonds at all if expectations are for higher interest rates? In this example, each year that interest rates go higher, the hypothetical portfolio would throw off more income, as it can reinvest maturing securities in higher yielding bonds, providing more cushion as interest rates increase further. There is a chance that none of the policy prescriptions President Trump has proposed are implemented as expected, that they don’t work as planned, or that President Trump focuses more on policies that are negative for growth, like trade protectionism, than the markets currently expect. There is also the risk that exogenous events, such as a further economic slowdown in China, eclipse the effects of good fiscal domestic policy. Finally, longer-term deflationary or disinflationary trends, including aging demographics, technological advancements, and unsustainable national debt levels, could happen faster than most investors expect, keeping the 35-year bull market in bonds charging for the foreseeable future.

In this era of radical uncertainty, the best portfolio defense is true diversification. A portfolio of well-researched, investment-grade municipal and corporate bonds continues to make sense as an important part of a balanced portfolio.

Editor’s note: This article is excerpted from a paper published by Evercore Wealth Management in February and an update in March following the defeat of the Republican efforts to repeal and replace the Affordable Care Act. To read the articles in full, please visit evercorewealthandtrust.com.

Brian Pollak is a Partner and Portfolio Manager at Evercore Wealth Management. He can be contacted at [email protected]. Howard Cure is the Director of Municipal Bond Research at Evercore Wealth Management. He can be contacted at [email protected].