Independent Thinking®

Now What? Time to Revisit Goals

March 3, 2022

Here’s a paradox: In the two years in which we have wrestled with a global pandemic and its myriad related issues, the S&P 500 soared, rising 120% from the initial shutdown shock. Now, just as the virus may be downshifting to endemic, the market and world is becoming more volatile.

There are reasons for this contradiction, of course, notably the recent spike in inflation and the prospect of rising interest rates, which are addressed in this issue of Independent Thinking – and now a major geopolitical shock in eastern Europe. But over the years, we have learned a thing or two about change. That’s why we work to construct flexible wealth plans and resilient portfolios intended to limit drawdowns and to produce reasonable, risk-adjusted returns, in all market conditions.

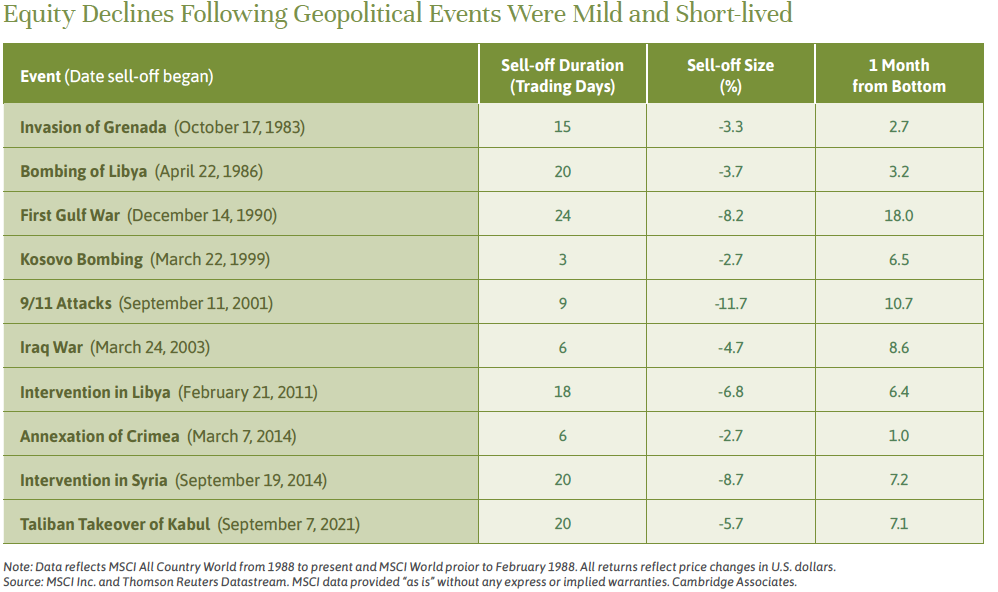

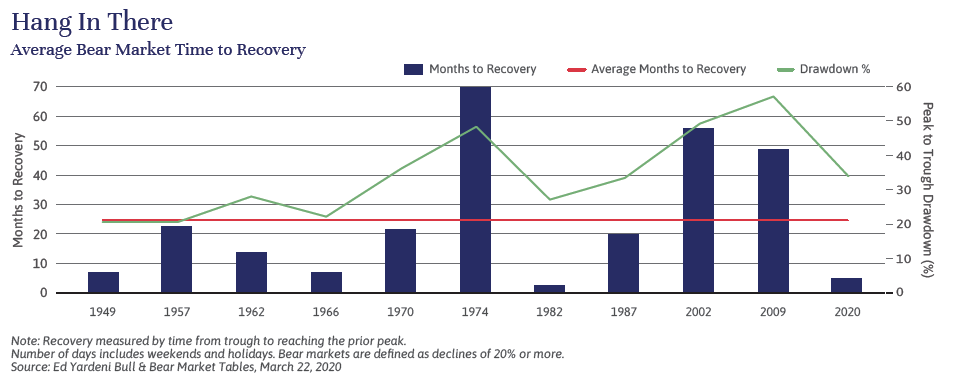

The first and most important step for investors is to acknowledge that these are challenging times and hang in there, come what may. Equity markets generally recover as the world returns to order, illustrated below.

Second, and specifically to investing, let’s deal with this change in the full context of our decade of remarkable gains. Thanks to a rare show of partisan resolve and an accommodating Federal Reserve, the U.S. economy barely missed a beat throughout the pandemic, and investors enjoyed spectacular stock market growth. Those of us who are retired or working remotely and sheltering in our own homes saw our balance sheets improve dramatically. We spent less and saved more, while our assets, including the homes in which we sheltered, soared in value.

As we look ahead and deal with this market correction, along with a period of inflation and rising interest rates, it is important to take the time to reexamine goals and appetites for risk and liquidity. As I talk with our clients, some common themes emerge. Here’s an example:

A couple, let’s call them the Smiths, had $20 million in liquid assets when they began working with us in our New York office in 2017, when the S&P 500 was less than 2,500. They were comfortable with some degree of risk but were willing to forfeit some prospect of return to protect their portfolio against substantial market drawdowns – an approach that kept them sanguine during the COVID-19 drawdown, illustrated below. In keeping with their risk tolerance, we continued to actively rebalance their portfolio, trimming equity gains as tax-effectively as possible, while adding to defensive and illiquid asset allocations. They have spent about 5% of their portfolio a year, but the market has more than made up for that, and they now have $25 million in investable assets even after the S&P 500 has fallen close to the 4,200 level in the current market drawdown.

As we recently sat down with the Smiths to review their accounts and our investment outlook, we came to the joint realization that they can now afford to explore more options, even taking into account the current volatility. The overall growth in their assets over the past five years has made them confident about their own future, able to withstand and exploit market fluctuations. They are now considering using a portion of their unified gift and estate tax credit and giving a portion of their still very appreciated securities to their children and grandchildren, letting the funds recover and grow for the next generation free of future estate tax. They can hedge their gifting through a Spousal Limited Access Trust, or SLAT, which would enable them to remove the assets from their taxable estate while allowing one spouse to have future access to the trust funds.

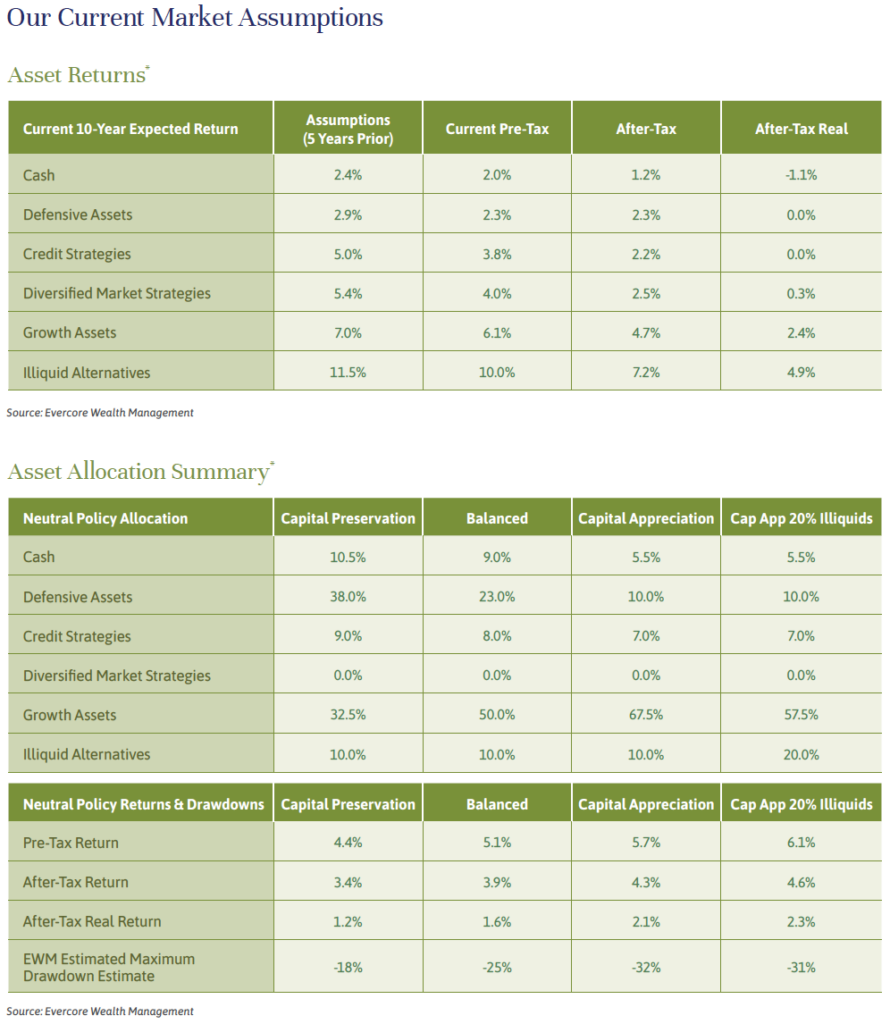

It’s important to note that the Smiths are able to consider taking on a little more illiquidity risk because they have over 25% of their portfolio in cash and defensive assets, enough to cover spending and capital calls for five years. Based on our capital market assumptions, we believe investing in illiquid growth opportunities can produce returns that exceed liquid growth equities by 3%-4% annually. The Smiths are also prepared to put some of their cash to work now, adding to quality shareholdings at more advantageous prices.

Of course, the right plan and the right investment portfolio will be as unique as the family it serves. The Smiths are considering taking on more risk. For others, sitting tight or taking less risk may be the appropriate solution at present. But I hope that all of us who are living through this extraordinary, paradoxical time will consider a thoughtful review now with trusted advisors.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at [email protected].

These assumptions made here include projections or other forward-looking statements regarding future events, targets, intentions or expectations. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements. There is no guarantee that projected returns or risk assumptions will be realized or that an investment strategy will be successful. No representation, warranty or undertaking is made as to the reasonableness of the assumptions made herein or that all assumptions made herein have been stated. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this document, will be profitable, equal any corresponding indicated performance level(s), or be suitable for your portfolio. The expected performance results do not reflect the impact that material economic and market factors may have on Evercore Wealth Management’s future decision-making. Model performance results cannot completely account for the impact of financial risks associated with actual market conditions. These returns should not be considered as indica tive of the skills of the investment adviser. A client’s actual return will be reduced by the advisory fees and any other expenses which may be incurred in the management of an investment advisory account.

Estimates for each asset class are based on proprietary Evercore Wealth Management research and both historical return data and on various forward looking forecast from accepted government agencies and private forecasters. 10-year return forecast is based upon a balanced account asset allocation. Returns are based on the these assumptions. After-Tax assumptions: Cash and Credit Strategies taxed at ordinary income rate. Defensive Assets are exempt from taxes. Growth Assets taxed at long-term capital gains rate. Diversified Market Strategies is taxed at a weighted average rate of 25% capital gains and 75% ordinary income. Illiquid Assets is taxed at a weighted average rate of 25% ordinary income and 75% capital gains. After-tax real returns are net of inflation. The maximum drawdown metric refers to the worst-case scenarios for a trading period, usually between a peak and trough for the market, including the following events: +200bps parallel shift in U.S. Treasury curve, +300bps parallel shift in credit spreads (OAS), 40% decline in global equity markets and +300% increase in the VIX Index. Asset class allocations may change. Returns are based on performance of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison. In addition, the Advisor’s recommendations may differ significantly from the securities that comprise the indices. Please consult your Evercore Wealth Management advisor for additional information.