Brian is a Partner and Portfolio Manager at Evercore Wealth Management, managing investments for families, foundations and endowments. He is the Chair of the Investment Policy Committee and co-Chair of the Asset Allocation Committee. He is co-head of the New York Office, Head of the Fixed Income Team and a member of the firm’s national Strategic Planning Committee. Brian additionally serves as Chief Investment Officer of Evercore Trust Company, N.A.

Brian joined Evercore in 2009 from AIG Investments where he co-managed over $60 billion in corporate bond portfolios. Brian earlier served as a corporate bond analyst, focused on basic industries, including paper/forest products, chemicals, and packaging companies. Prior to attending business school, Brian worked for the Milken Family Foundation.

Brian received his B.A. in History from the University of Pennsylvania and his M.B.A. in Finance from Columbia University. He holds the Chartered Financial Analyst designation and is a member of the CFA Institute.

Shaking it Off: The Markets and Geopolitical Crises

When all the world seems to be going to hell, what should a prudent investor do? Hold tight or buy seems to be the answer, in most situations. For those with a long-term term horizon, equity investments made right before times of geopolitical stress generate returns roughly in line with long-term averages. And those made shortly after the time of the initial shock often realize outsized returns.

That’s not an argument for trying to time the market. That rarely works, as most investors struggle to time both the sale and the repurchase of stocks – and even perfect market timing barely outperforms buying and holding. But it is an argument for staying calm and focusing on long-term goals.

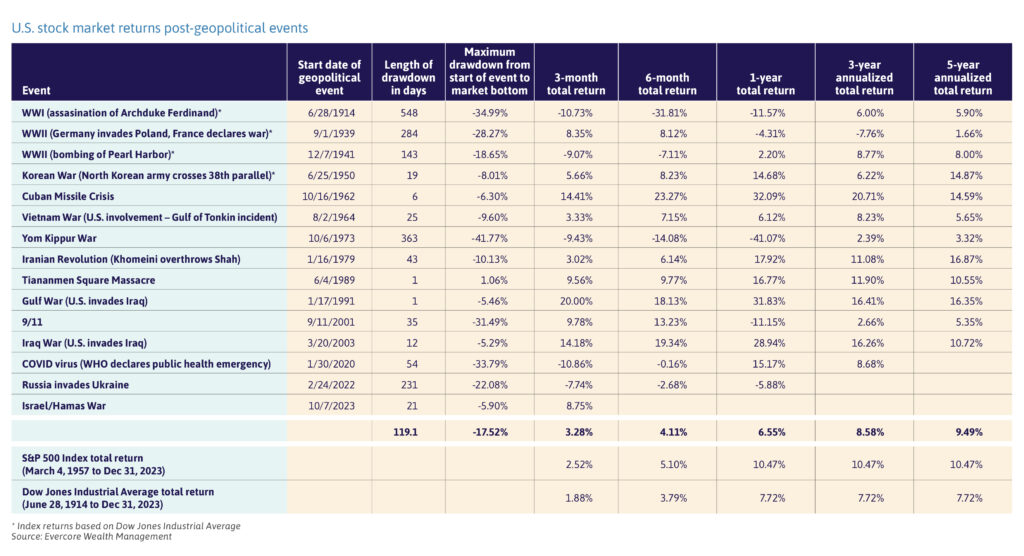

Look at the data. U.S. equity returns since World War I (as measured by the Dow Jones until 1957 and the S&P 500 thereafter) rode out revolutions, terrorist attacks and global pandemics. But not immediately: The initial drawdown averaged 17.5% and nearly 120 days, as illustrated below. But average returns across these events over the subsequent six months, and one, three and five years were all positive (see the chart below). Clearly, longer-term market returns during periods of geopolitical upset are most related to the underlying economic conditions and valuations at the time.

The 1950s and 1960s were generally robust economic times in the United States. Consequently, the markets rose steadily, even after the outset of a hot war in Korea and through the rising Cold War tensions that culminated in the Cuban Missile Crisis, a threat that felt existential to many. The markets were recovering from a decade of high inflation when the Shah of Iran was overthrown in 1979 – and they continued to do so.

Conversely, the markets were still reeling from the dot.com crash ahead of the 2001 attacks on the United States. Consequently, the sharp selloff when U.S. markets reopened on September 17 after a seven-day suspension was only a small part of the story, as the tech-led bear market was at that point only part way toward its bottom – eventually hitting its nadir in October 2002. And during the global COVID-19 pandemic, which generated many geopolitical consequences, investors quickly turned their attention to the tech and productivity boom. The S&P 500 plunged 34% when the outbreak reached the United States, then it rose 65% over the remainder of 2020.

So, what are the exceptions to this market sangfroid? Or rather, what are the conditions that make for exceptions? And are the hot wars waging in Europe and the Middle East, the coming U.S. election, or something else in the works potential candidates for long-term disruption? Events that have changed or can change the trajectory of global economic growth and/or inflation, and therefore corporate earnings, are the ones that can cause long-term damage in the markets. They are few and far between, but the damage is generally considerable. In these cases, investors’ time horizons would have to be long, as the drawdowns lasted a year or more, and market returns for even three and five years were well under expectations. But again, long-term investors were generally better off staying in the market.

The two world wars, to take the most obvious examples, changed the course of trade, production, and the labor force for a large portion of the globe. The U.S. stock market, then best measured by the Dow Jones Industrial Average, took 18 months to recover from the start of the “War to End All Wars”. Twenty-four years later, in 1939, the Dow Jones actually rose 15% over the seven trading days after Germany’s invasion of Poland, as investors bet that U.S. corporations would benefit from selling arms and other goods to the European combatants. Reality had set in by 1940, when Germany overran Belgium and France, signaling that the war would be long, and would include the United States. Interestingly, the market began its rebound just a few months before the Battle of Midway, in June 1942, a sign perhaps that the investors in aggregate this time around were able to intuit the eventual outcome, well before many of the pundits of the day.

Another example of a geopolitical conflict that caused significant economic and market disruption was the 1973 Arab-Israeli War, also known as the Yom Kippur War. The related oil embargo imposed by the Arab Organization of Petroleum Exporting Countries, or OPEC, hit the United States economy where it hurt, and the S&P 500 lost over 40% in the following 12 months. It is important to note that this is unlikely to happen today, at least not in the United States, which is now energy independent and a net exporter of petroleum products.

At present, we have no reason to count either the war in Ukraine or the Middle East, as horrific as they are, among the few events in which the appropriate response would be to sell or to take on the expense of hedging equity portfolios. That’s true too for the coming and remarkably unpopular U.S. election. One potential long-term disrupter that does come to mind is a Chinese invasion of Taiwan, home to most of the world’s high-value semiconductor manufacturing. To us, this seems a possible but not probable event, and one that can best be protected against through appropriate portfolio diversification.

For long-term investors, there have been very few political shocks to which the appropriate response would have been to sell equities. Let’s hope it stays that way.

Brian Pollak is a Partner and Portfolio Manager at Evercore Wealth Management. He can be contacted at [email protected].

This Independent Thinking® issue explores the challenges and opportunities of managing investment portfolios amid buoyant but increasingly volatile markets. It discusses the risks of market peaks, the potential for inflation