John is the Chief Investment Officer of Evercore Wealth Management, responsible for the firm’s market outlook and asset allocation policy. He has over 30 years of experience managing balanced investment portfolios for high net worth clients and foundations and endowments.

Prior to joining Evercore in 2008, John was a managing director of U.S. Trust, which he joined in 1984. He was responsible for managing $2 billion of client assets, representing many of U.S. Trust’s most significant clients. Additionally, John served as the Chief Investment Officer of U.S. Trust of New York from 2003 to 2005, and as the head of Equity Investments and the Chair of the Equity Investment Committee from 2005 to 2008. For 15 years, he was an active participant in the formulation of overall investment strategy and a member of the U.S. Trust Investment Strategy Committee.

Prior to attending business school, John was on the staff of the U.S. Senate Labor and Human Resources Committee and worked on federal budget matters.

John received his B.A. from Bucknell University and an M.B.A. from New York University. He holds the Chartered Financial Analyst designation and is a former member of the Board of the New York Society of Security Analysts.

“First, do no harm.” Interestingly, that line is not part of the Hippocratic oath, although it is attributed to the ancient Greek physician. It’s also not always practical; if we followed it, we would never have surgery, for example. The expression has resonated through the ages because it suggests a balance.

President Trump is trying to rebalance world trade and the interrelated financial system. Since the United States quit the gold standard in 1971, Americans have enjoyed what a former French finance minister described as our privilege exorbitant, in controlling the world’s reserve currency. The U.S. dollar is the most widely held asset by foreign central banks, the most widely used currency for foreign trade, and the currency of choice for many countries to borrow in. When Japan buys oil from Saudi Arabia, it pays in dollars; when Vietnam buys German machinery, it pays in dollars; when Argentina issues bonds on the world market, they are denominated in dollars. Global growth runs on the greenback.

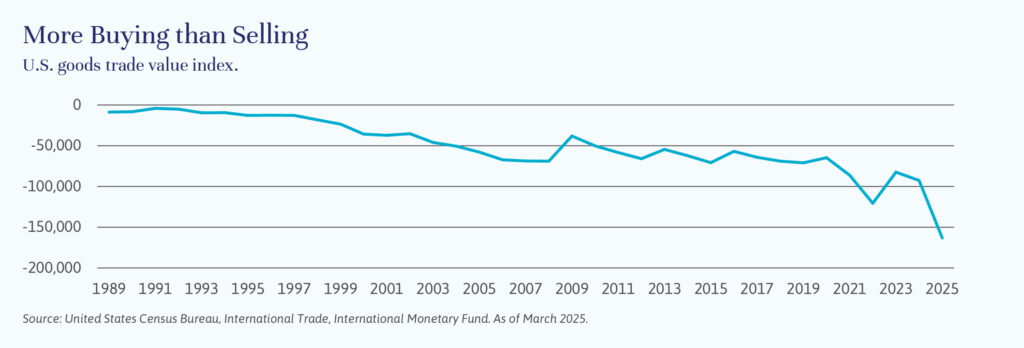

Access to all these dollars is facilitated by a persistent imbalance in the trade of goods between the United States and most of its trading partners. (The United States has a trade surplus in services and has benefited, along with the rest of the world, through the global growth generated by free trade.) But dollars sent overseas do not disappear. Instead, they are invested in U.S. dollar assets, including U.S. government bonds. This support has enabled the U.S. federal government to run ever larger deficits with higher debt levels without stressing the market.

In short, the global demand for dollars, our great privilege, has until recently kept the value of the dollar high. This currency strength has enabled U.S. consumers to buy foreign goods cheaply and enabled emerging markets to build up manufacturing bases to meet that demand, lifting millions of people out of poverty.

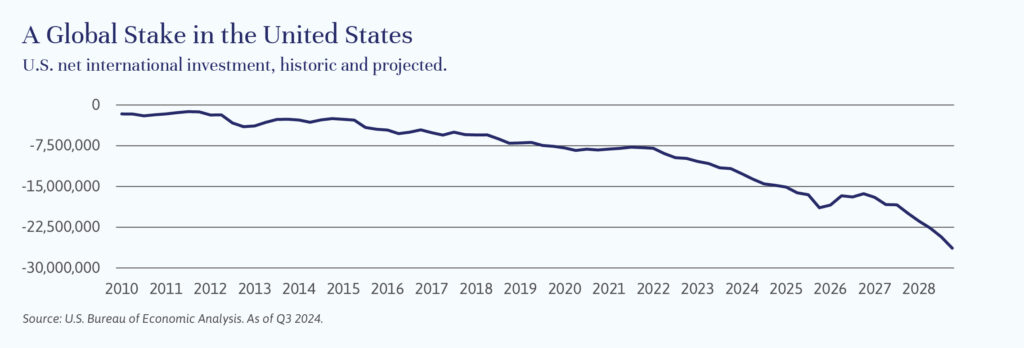

Has it all been too much of a good thing? Clearly, this administration thinks so. As a result of all the additional dollars invested back in U.S. dollar assets – including public equities, government and corporate bonds, real estate and direct investments in plants and equipment – the United States has an increasingly unbalanced investment position. Foreign entities own far more U.S. assets (a net $26 trillion) than U.S. investors own foreign assets. (See the chart “A Global Stake in the United States”.)

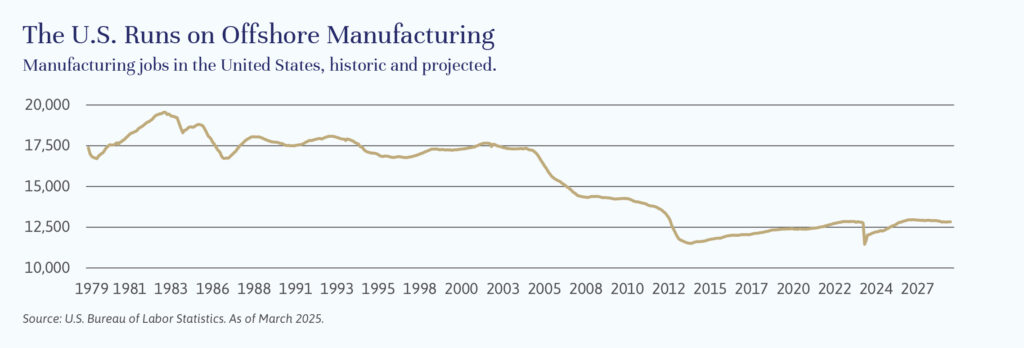

An additional consequence of the current system is that American workers and communities dependent on U.S.-based manufacturing are suffering. And we have become dependent on foreign-made supplies of many strategic items, including manufactured goods and materials necessary to build up and replace armaments and other military equipment. Addressing these issues through onshoring will take considerable effort and time and investment – and will not be economically advantageous in many cases.

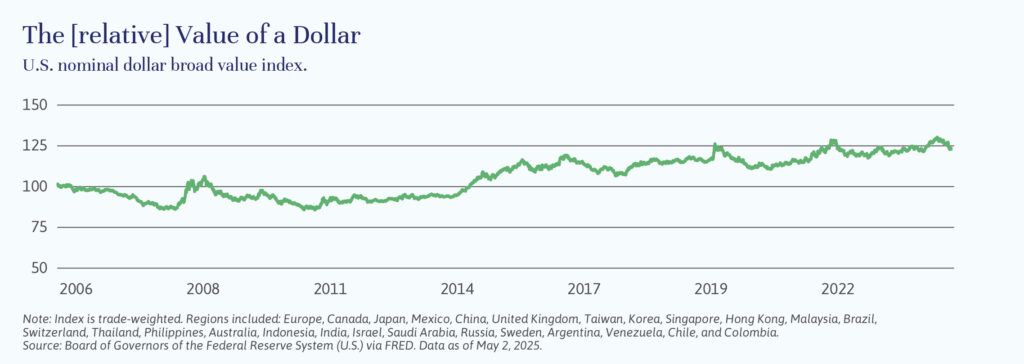

A managed devaluation of the dollar has been tried in the past. (See the article by Brian Pollak “A Brief History of Reserve Currencies“.) The efforts this time so far are more like a shock treatment. Very high and erratic tariffs and related threats are making the patient worse. The U.S. dollar is falling now, but possibly for the wrong reasons. After a dizzying spate of contradictory announcements from President Trump, the world is questioning the basic assumptions that have underpinned its reserve currency status – the economic vitality and political stability of the United States, along with our commitment to the rule of law, defense guarantees, and our responsible, independent central bank.

While we continue to expect that the extreme tariff rates will be reduced, partly in response to market reaction, and that the dollar will decline more gradually, there is now an increased probability that the United States and much of the world will enter a recession.

We are managing portfolios with these heightened risks in mind. In uncertain times, it is imperative that portfolios are well diversified. Our clients have benefited from being overweight U.S. public equity – and those gains are now being rebalanced in favor of international equities, as well as private equity where appropriate (see the article by Stephanie Hackett on “Buying, Building and Selling: Investing in Private Equity“) and public and private credit. These asset classes provide further diversification and, in the case of credit, enhanced income. Additionally, there should be sufficient cash and short-term bonds in portfolios to fund spending needs for two years or more.

John Apruzzese is the Chief Investment Officer of Evercore Wealth Management. He can be contacted at [email protected].

This Independent Thinking® issue explores the challenges and opportunities of managing investment portfolios amid buoyant but increasingly volatile markets. It discusses the risks of market peaks, the potential for inflation