Brian is a Partner and Portfolio Manager at Evercore Wealth Management, managing investments for families, foundations and endowments. He is the Chair of the Investment Policy Committee and co-Chair of the Asset Allocation Committee. He is co-head of the New York Office, Head of the Fixed Income Team and a member of the firm’s national Strategic Planning Committee. Brian additionally serves as Chief Investment Officer of Evercore Trust Company, N.A.

Brian joined Evercore in 2009 from AIG Investments where he co-managed over $60 billion in corporate bond portfolios. Brian earlier served as a corporate bond analyst, focused on basic industries, including paper/forest products, chemicals, and packaging companies. Prior to attending business school, Brian worked for the Milken Family Foundation.

Brian received his B.A. in History from the University of Pennsylvania and his M.B.A. in Finance from Columbia University. He holds the Chartered Financial Analyst designation and is a member of the CFA Institute.

Gold could be considered the first reserve currency. The first gold coins that we know of were struck around 550 BC, initiating a measure of value and facilitating trade and transactions between different groups of people – even those from different regions and cultures – that has lasted to this day. Gold remains a monetary asset to this day, never entirely losing its luster.

Spanish silver dollars, also known as Spanish Pieces of Eight, and Dutch guilders are now collector items. But each also had their time in the sun. Pieces of Eight emerged in the 16th century as the first reserve currency associated with a sovereign nation. The coins were uniform in weight and silver content, making them a reliable medium of exchange as Spanish ships traveled around the world. The Bank of Amsterdam, established in 1609 and often considered the precursor to modern central banks, was the first public bank to offer accounts that were not directly convertible to coin, creating a new and easier form of transferability and liquidity. This innovation supported the use of the Dutch guilder as a global currency, as did the simultaneous rise of the Dutch East India and Dutch West India trading companies, which expanded global trade throughout Asia and the Americas.

By the 19th century, trade and capital investments were often denominated in sterling. Britain’s dominance in technology, innovation and production allowed its goods to be sold around the world and created the need for large quantities of raw materials and natural resources. Sterling weakened substantially through the world wars, when Britain took on significant debt and exhausted its foreign reserves. Nevertheless, it maintained an important position in global trade and as a reserve currency for much of the world until the end of World War II, when the sun finally set on the British empire.

Enter the U.S. dollar. The U.S. manufacturing base, unscathed by the Great War, became a producer of goods for all of Europe, including the United Kingdom, helping to elevate the dollar to a global currency. In addition, the U.S. dollar generally remained a hard-backed currency during this period, while many European currencies of the day, including sterling, did not. (The United Kingdom went off the gold standard from 1914 to 1925 and then permanently in 1931.) U.S. dollars poured into Europe and Japan after World War II to rebuild and redevelop shattered economies and infrastructures.

The Bretton Woods conference of 1944 codified the role of the U.S. dollar as the foundation of the global financial system. Here, most global currencies were officially pegged to the dollar, which was pegged to gold at a fixed exchange of $35 an ounce. The World Bank and the International Monetary Fund were established as well, all with a goal of stabilizing the post-war global economy.

It was, without a doubt, the American century. But there were two significant currency events since Bretton Woods, both provoked by large global trade imbalances.

The first was the so-called Nixon Shock of August 1971, in which the United States broke the Bretton Woods agreement by ending the convertibility of dollars to gold. The country was then running significant (although small by today’s standards) twin trade and fiscal deficits. Americans were buying a lot of West German and Japanese goods (the trade deficit) while funding the Vietnam War and the Great Society programs (the fiscal deficit). At the same time, many central banks were converting their dollars into gold, draining U.S. gold reserves, while the United States kept printing dollars without enough gold reserves to back those dollars.

Leaving the gold standard solved the problems of the day, weakening the dollar and rebalancing trade, at least for a time. It also gave global central banks, including the U.S. Federal Reserve, more autonomy over monetary policy, allowing most global currencies to float freely. But it made the dollar a fiat currency, wherein the value of a currency is derived from trust, not by the backing of a physical metal. This has caused the devaluations of less powerful currencies, such as the Argentinian peso, and many more currency crises. Some economists believe that those monetary policy actions were at least part of the reason for the stagflation (slow growth and high inflation) that persisted in the United States through much of the 1970s.

The second major intervention was the Plaza Accord of September 1985. In the years prior, the dollar had appreciated significantly against other major currencies, largely due to the relatively high interest rates implemented by Federal Reserve Chair Paul Volker to fight inflation. The recovered strength of the dollar had made U.S. goods more expensive to export and foreign goods cheaper to import, leading to another large trade deficit, again with West Germany and Japan. The Plaza Accord participants (the G5 – the United States, the United Kingdom, Japan, West Germany and France) agreed to work toward weakening the U.S. dollar, specifically in relation to the Japanese yen and German deutsche mark. The Accord essentially worked, leading to a lower dollar and a narrowing of trade imbalances. By 1987, the Louvre Accord was struck, essentially reversing the Plaza Accord, ending the period of dollar weakness and stabilizing the global currency markets.

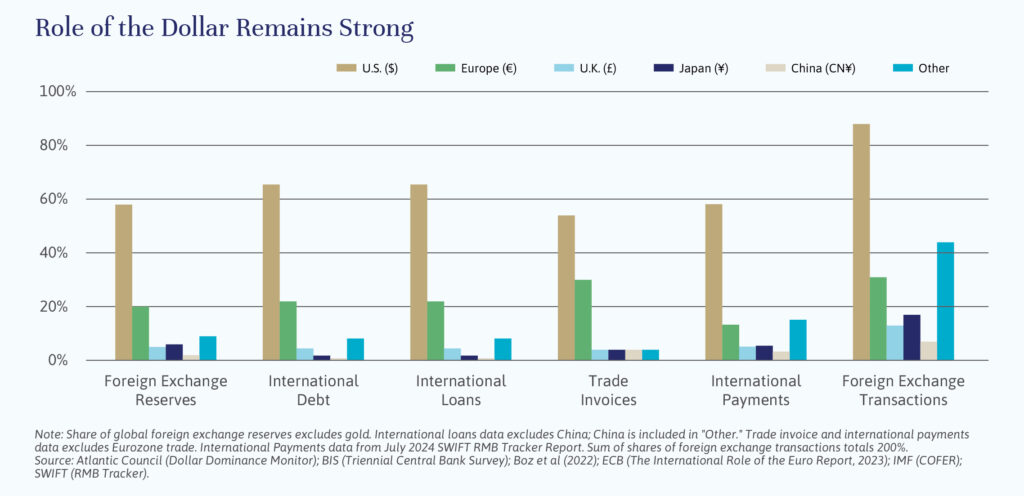

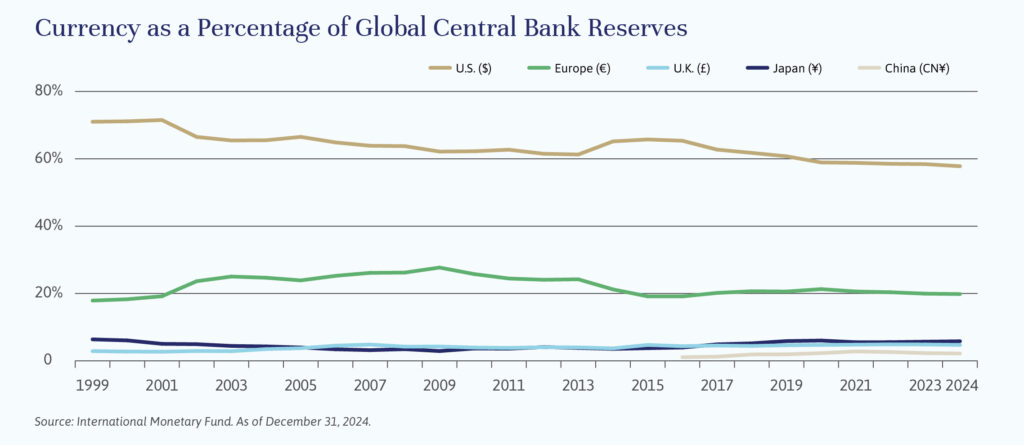

Will the Trump administration’s attempts to weaken the dollar constitute another major dollar intervention? It’s too early to say. The fiscal and trade imbalances of today are more significant than those of either 1971 or 1985, but the economy itself is in better shape, and the dollar continues to benefit from global trust in the United States, as illustrated in the chart “Role of the Dollar Remains Strong”. Still, there are already signs that the dollar is fraying. Its share of global central bank reserves fell 13% over the past 25 years as others grew, primarily the Euro but also the yen, sterling, and the Chinese yuan. (See the chart “Currency as a Percentage of Global Central Bank Reserves”.) And gold, the original reserve currency, still plays an important role 2,500 years on. International debt, currency denominations, international trade and foreign exchange transactions tell a similar story.

It is reasonable to predict that the dollar continues to erode, ceding more of its dominance as the global currency. The difference this time is that there is no single alternative currency waiting in the wings, at least not yet. The Euro suffers from still uncoordinated fiscal policies; the yuan is still a highly managed currency, currently kept deliberately low by the Chinese government; and the yen suffers from demographic challenges and very low interest rates. Digital assets like Bitcoin are nascent and highly volatile. Stablecoins are a more likely potential solution, but digital assets pegged to one or more fiat currencies remain in a very early stage of development. And gold, while shining bright at present, is not a scalable alternative. For most U.S.-domiciled investors, who will want to match dollar liabilities with dollar assets, diversification away from the dollar makes sense only incrementally.

Brian Pollak is the Head of the Investment Policy Committee at Evercore Wealth Management. He can be contacted at [email protected].

This Independent Thinking® issue explores the challenges and opportunities of managing investment portfolios amid buoyant but increasingly volatile markets. It discusses the risks of market peaks, the potential for inflation