Brian is a Partner and Portfolio Manager at Evercore Wealth Management, managing investments for families, foundations and endowments. He is the Chair of the Investment Policy Committee and co-Chair of the Asset Allocation Committee. He is co-head of the New York Office, Head of the Fixed Income Team and a member of the firm’s national Strategic Planning Committee. Brian additionally serves as Chief Investment Officer of Evercore Trust Company, N.A.

Brian joined Evercore in 2009 from AIG Investments where he co-managed over $60 billion in corporate bond portfolios. Brian earlier served as a corporate bond analyst, focused on basic industries, including paper/forest products, chemicals, and packaging companies. Prior to attending business school, Brian worked for the Milken Family Foundation.

Brian received his B.A. in History from the University of Pennsylvania and his M.B.A. in Finance from Columbia University. He holds the Chartered Financial Analyst designation and is a member of the CFA Institute.

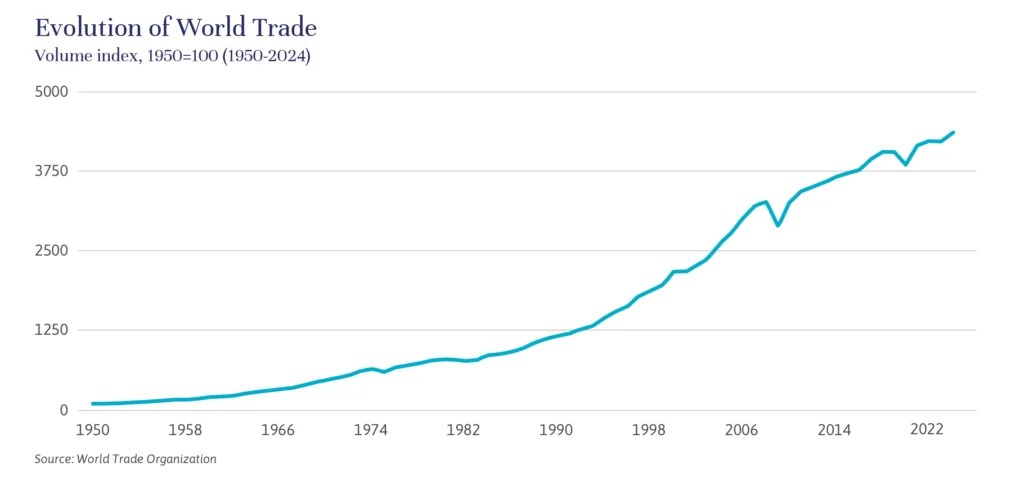

In the waning years of his presidency, Bill Clinton said this: “Globalization is not something we can hold off or turn off. It is the economic equivalent of a force of nature, like wind or water.” Twenty-five years on — through a pandemic, war in Europe and the Middle East, various natural disasters, protectionist rhetoric around the world, and even with the disruptive and still uncertain tariff policy in the United States — his theory still holds up.

Global trade in 2025, both in goods and services, is expected to end at all-time highs. Shipping lanes still stretch around the world, carrying every manner of goods, even as the two global powerhouses distance themselves from each other. But the cargo carrier flags are changing as the United States and China seek more closely aligned trading partners — not geographically, but philosophically and politically — and reshape their critical supply chains accordingly.

As our Evercore ISI colleague Neo Wang describes in his article “China: Moving Up the Value Chain”, China is now exporting advanced goods as well as influence around the developing world through its Belt and Road Initiative. Meanwhile, the United States and its allies are increasingly focused on the origin of certain critical goods and services — including semiconductors and other edge computing technologies, key natural resources, high-capacity batteries, pharmaceuticals, the latest aerospace and defense technologies, and sensitive financial, technology consulting, business, and legal services.

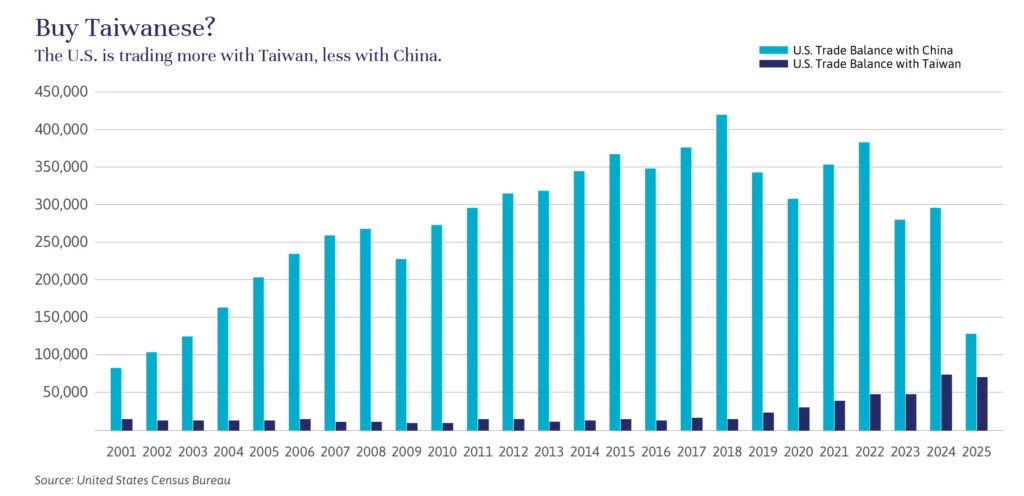

As a result, we expect trade in these critical goods between the U.S. and China to continue to decline. At last count, the U.S. trade deficit with China stood at $295 billion — a 30% fall since its peak in 2018. It is projected to fall further by the end of this year, back to levels last seen in 2005, shortly after China joined the World Trade Organization, or WTO, in 2001, and shortly before China became the world’s biggest exporter of goods in 2009 and the world’s largest trading nation five years later.

Meanwhile, U.S. trade with Taiwan — still home to an estimated 90% of the world’s high-end semiconductor manufacturing — has soared, with imports to the U.S. doubling between 2019 and 2024 and expected to rise further in 2025. The chart “Buy Taiwanese” serves as a reminder of how dramatic the ebbs and flows of the past two decades have been.

Foreign direct investment, or the purchase of an ownership stake in an asset by a foreign government, company, or investors, is declining — notably in natural resource extraction — amid a desire by countries to exert greater control over their own energy infrastructure. As Neil Shearing posits in his excellent book The Fractured Age, the Russian invasion of Ukraine in February 2022 forced Europe to rethink its energy supply chain. Prior to the war, Russia supplied the European Union with 40% of its natural gas and 30% of its oil. The European Union has since turned off the Russian tap, importing instead from the United States, Norway, and Brazil. Meanwhile, Russia continues to export to China and the still relatively unaligned India and Turkey. The war did not diminish global trade — it contributed to reorienting it.

But cross-border merger and acquisition activity and new foreign direct investment into high-tech areas such as semiconductor manufacturing remain robust (see sidebar “Semiconductors: Chips on the Trade Table”), as nations with aligned interests invest in infrastructure to help diversify their allies’ supply chains and manufacturing bases. This is likely to be bolstered by recent trade deals that included commitments, notably from Japan and Korea, to invest in the U.S.

In a world that appears increasingly divided into two camps, globalization can continue to grow. The economic law of comparative advantage — the idea that one country can produce a good or service at a lower opportunity cost than another — still applies. Apparel, toys, and certain commodities are all likely to continue trading relatively freely. More sensitive goods will be “friend-shored,” manufactured in and imported from reliable allies. It is worth noting that the U.S. maintains a large trade surplus in services, which is likely to continue, and that the U.S. economy is much less exposed to the trade of goods, due primarily to its massive services sector, which at about 79% of GDP is by far the highest in the world.

We do not anticipate this reorientation of trade to have a large impact on global GDP. It’s still globalization — just not as we knew it. However, as long-term investors, we attempt to look through the vagaries of current policy and related market disruptions to the potentially more lasting impacts on individual companies, sectors, regions, and countries.

As with any reorientation, there are risks — the biggest of which is a military conflict between the United States and China over Taiwan. While we see this as having an extremely low probability today, as the two economies become less integrated, this risk could rise. A second risk is that the United States is at the beginning of a longer-term retrenchment from its traditional allies, which, if persistent, would diminish the country as an economic power and accrue to the benefit of China. It could also spur Europe and Japan to bolster their own domestic technological prowess, furthering the regionalization of global supply chains and trade.

And of course, there are opportunities. Companies and sectors of the economy that have built or are building supply chains positioned to serve the newly oriented global trade routes are potential winners, as are those with access to relatively cheap labor or specific technical proficiency. We continually assess the changing global landscape as we consider both risks and opportunities within our current and new potential investment recommendations.

We believe globalization remains a force but anticipate continued change in its flows and impact — and rising volatility as the markets react to that change. We evaluate these changes and the related potential risks and opportunities, to provide context for our fundamental analysis of the securities and funds, private and public, that we invest in on behalf of our clients. We believe that diversification remains the best defense against tariff policy swings and macro surprise.

Semiconductors: Chips on the Trade Table

Reshoring semiconductor manufacturing in the United States has been a policy focus for years, through both the Trump and Biden administrations. Major legislation (the CHIPS Act and the Inflation Reduction Act), export controls, and tariff policies have all maintained that focus.

While the United States dominates semiconductor design — led by Nvidia and followed by AMD and Broadcom — and many semiconductor fabrication plants are under construction in the U.S., it will likely take decades to build both the manufacturing and technical human capital capacity to support domestic demand for high-end chips. That leaves just one company, TSMC of Taiwan, producing the lion’s share of advanced chips, and most of that in Taiwan. The equipment needed to produce those chips — the most advanced lithography machines used to etch intricate circuit designs onto silicon wafers — are also made solely by one company: Netherlands-based ASML.

Coordinated export controls by the United States, Taiwan, the Netherlands, and other U.S. allies have severely restricted China’s access to this critical technology. As Neo Wang describes, China has undertaken a Herculean — and relatively fast and successful — effort to recreate the semiconductor supply chain domestically. While Chinese-made semiconductors are likely two generations behind those produced by the U.S. and its allies, China is both making do and catching up — propelling the country into higher-end manufacturing and enabling it to export these chips to its own closest allies.

There will still be plenty of semiconductors and related equipment crossing borders (and related investment opportunities), just less so between the United States and China.

—BP

Brian Pollak is the Chair of the Investment Policy Committee at Evercore Wealth Management. He can be contacted at [email protected].

This Independent Thinking® issue explores the challenges and opportunities of managing investment portfolios amid buoyant but increasingly volatile markets. It discusses the risks of market peaks, the potential for inflation