John is the Chief Investment Officer of Evercore Wealth Management, responsible for the firm’s market outlook and asset allocation policy. He has over 30 years of experience managing balanced investment portfolios for high net worth clients and foundations and endowments.

Prior to joining Evercore in 2008, John was a managing director of U.S. Trust, which he joined in 1984. He was responsible for managing $2 billion of client assets, representing many of U.S. Trust’s most significant clients. Additionally, John served as the Chief Investment Officer of U.S. Trust of New York from 2003 to 2005, and as the head of Equity Investments and the Chair of the Equity Investment Committee from 2005 to 2008. For 15 years, he was an active participant in the formulation of overall investment strategy and a member of the U.S. Trust Investment Strategy Committee.

Prior to attending business school, John was on the staff of the U.S. Senate Labor and Human Resources Committee and worked on federal budget matters.

John received his B.A. from Bucknell University and an M.B.A. from New York University. He holds the Chartered Financial Analyst designation and is a former member of the Board of the New York Society of Security Analysts.

How can we assess value when record-high stock valuations are being driven by bold bets on the rapid deployment and monetization of Artificial Intelligence, or AI? While we believe equities will continue to outperform other liquid assets over the long term, it’s impossible to know when — or even if — today’s expectations around AI will be realized.

Traditionally, we’ve looked to high-quality fixed income as a counterweight — a safe harbor during periods of “irrational exuberance,” a phrase coined two decades ago by then Federal Reserve Chairman Alan Greenspan, or in times of recession. But as we’ve discussed in previous editions of Independent Thinking, we can no longer assume that the U.S. dollar, or dollar-denominated securities, will reliably preserve value. Critical institutions are coming under attack and losing public confidence. The Fed risks eroding its hard-won independence — further undermining that confidence.

Meanwhile, the fiscal health of the U.S. government continues to deteriorate. Federal debt held by the public has climbed to roughly 100% of GDP and is still growing. Most troubling is the lack of political will — on either side of the aisle — to meaningfully reduce the deficit, even as it reaches levels historically seen only during wartime or severe recession. Despite the dollar’s recent decline — about 10% recently against other major currencies, notably the yen, pound, and euro — the greenback has been relatively strong over the last decade. This owes less to U.S. strength than to the weakness of peers. Global debt now exceeds 330% of GDP.

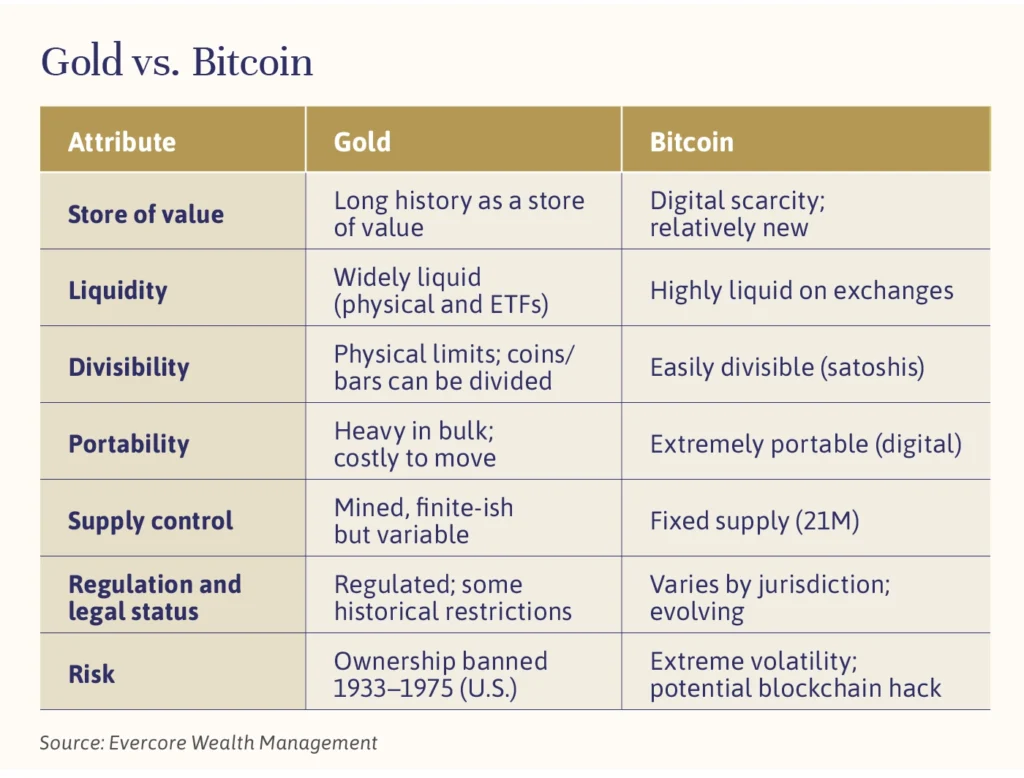

In addition to private equity (see the article by Stephanie Hackett, “The Case for Private Equity: The Evercore Wealth Management Private Equity Access Fund”), nonproductive stores of value — assets that generate no income but potentially preserve or enhance purchasing power outside fiat systems — look increasingly attractive. Gold, the quintessential physical asset, is not a hedge against equity bear markets; it is a hedge against the erosion of cash and dollar denominated fixed-income purchasing power. In this environment, it’s reasonable to expect gold to continue outperforming traditional defensive assets over the short to medium term, as it has for the past three years.

Bitcoin may represent another form of nonproductive value storage. Its existence is brief compared with gold’s millennia-long history, yet its value has grown rapidly as global demand growth has outstripped supply, which is finite by design. While Bitcoin remains extremely volatile, the degree and duration of the swings appear to be diminishing. Acceptance of Bitcoin as a store of value is receiving a significant boost in the United States as the federal government clarifies a new, friendly regulatory regime that is integrating Bitcoin (and other parts of the crypto ecosystem) into the mainstream financial system.

It’s worth noting that stablecoins backed by the U.S. dollar are not a store of value in that context. Most of the use cases for Bitcoin to date have been in countries with flawed fiat currencies and/or underdeveloped banking and transaction services. As Bitcoin becomes firmly established, portability gives it practical advantages over gold.

Both assets historically exhibit reasonably low correlation to equities and bonds and support portfolio resiliency. During the crises of 2008 and 2020, gold acted as a hedge against systemic liquidity shocks; in recent equity market selloffs, Bitcoin displayed higher volatility but a faster recovery than stock indices. Even a modest allocation — we are recommending 3% gold and 1% Bitcoin weightings in appropriate accounts — can potentially enhance portfolio resilience. Gold has historically helped stabilize returns during drawdowns, while we believe Bitcoin should add convexity and long-term appreciation potential.

In essence, gold and Bitcoin are the historical and digital answers to the same question: How do investors protect wealth when trust in money erodes? In an era when fiat currencies are printed without restraint and real yields remain suppressed, scarce assets can provide meaningful diversification and preserve purchasing power over time.

John Apruzzese is the Chief Investment Officer at Evercore Wealth Management. He can be reached at [email protected].

This Independent Thinking® issue explores the challenges and opportunities of managing investment portfolios amid buoyant but increasingly volatile markets. It discusses the risks of market peaks, the potential for inflation