There’s a lot for investors to think about as we make our way into 2026. The markets have weathered multiple once-in-a-generation events in a single generation, including the dot.com bust, 9/11, the record losses of the great financial crisis and, of course, the pandemic. Yet those first 25 years of this century turned out to be one of the greatest, albeit uneven, wealth-creation periods in U.S. history. One in five Americans is now a millionaire; there are close to one million decamillionaires.1

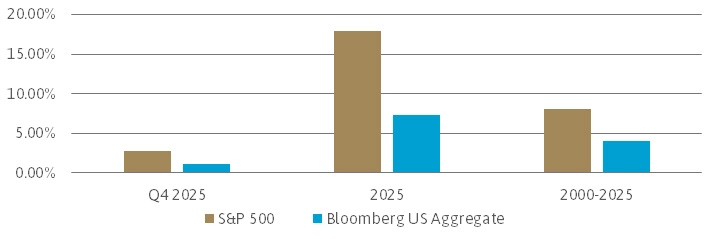

STOCK AND BOND RETURNS OVER SHORT AND LONG TIME PERIODS

Source: FactSet; Q4 2025 return is cumulative.

2025 saw the S&P 500 rise 17.9% but it meaningfully trailed international markets, with the MSCI ACWI ex-US up 33.1%, driven largely by a weakened dollar and improved valuations. Most bond markets rose, with the interest rate-sensitive Bloomberg U.S. Agg up 7.3% and credit-sensitive HY up 8.6%2. The price of gold soared, hitting all-time records, as central banks bolstered their reserves.

While investors experienced yet another year of robust gains, there are plenty of questions worth asking now.

1. Why Has Geopolitical Turmoil Not Impacted Markets? Will It?

Most geopolitical uncertainties generally don’t weigh long on the market, as investors tend to differentiate headline risk from economic risk that could affect earnings growth. Comments by President Trump that the United States will run Venezuela and needs Greenland have so far not affected markets adversely, nor have the ongoing conflicts in the Middle East and Ukraine.

2. What About U.S. Fiscal Policy and Debt?

Domestic fiscal and monetary policy is more meaningful in this context; and the outlook is mixed. The Administration’s tariff threats have come to be seen by investors as negotiable and incremental. Broader policy is still supportive of the markets.

Tax rebates, deregulation (mostly prominent in the energy and financial services industries) and additional Fed easing should all foster economic growth. DOGE made no real impact on fiscal spending, with total U.S. government outlays around $7 trillion in 2025, up about 6% from the prior year. Meanwhile, tariffs have had a modest impact on reducing the deficit. Debt levels relative to GDP are massive around the world, not just in the United States. But the U.S. debt load is more prevalent at the government level. Consumer and corporate debt/income ratios are relatively normal, making a traditional credit crisis unlikely.

3. Was 2025 the Beginning of the End of U.S. Market Dominance?

No, but the U.S. advantage is narrowing, as government debt and intervention in the corporate sector rises and the dollar loses value. And China is catching up quickly across key technology sectors, including AI, electric and autonomous vehicles, and even semiconductors. For now, the U.S. corporate sector still boasts superior earnings growth and maintains a significant technology lead – and the U.S. dollar remains the world’s reserve currency. We are increasing our exposure to international stocks but remain overweight the U.S. markets.

4. Is There an AI Bubble Forming?

We need to distinguish between a bubble with fundamental underpinnings and a speculative mania. Signs of an AI bubble are certainly present, including among some companies, circular financing, extreme valuations, and increasing debt loads to finance AI infrastructure. But a mania, which is characterized by a more extreme speculation far exceeding intrinsic value, is less in evidence. AI technology is real and adoption is broadening. AI-related capex is already a meaningful contributor to U.S. GDP growth and is fast becoming an important leg of U.S. infrastructure. As AI use cases grow, the cycle will continue into broader corporate productivity. For prudent investors this presents an opportunity to invest in companies with current and significant profits and relatively low debt and valuations.

5. Will The U.S. Consumer Continue to Hang On?

High income households, notably led by Baby Boomers, are benefitting disproportionately from the wealth effect of rising home and equity prices. They remain confident consumers. Lower-income and younger Americans remain constrained by the still-elevated prices of many day-to-day goods (partially due to higher tariff rates), higher electricity prices, and near-record low housing affordability. While aggregate consumer debt remains low, debt loads among this second group are rising, leading to higher delinquency rates. This partially explains why consumer sentiment remains as a whole so weak despite relatively strong economic data.

The labor market, with the unemployment rate at 4.4% through December, remains solid but is showing signs of weakness. Job growth has cooled, and companies appear reluctant to hire. But the labor pool itself is stagnating, partially due to lower net immigration. If this equilibrium holds and more Baby Boomers retire, we could see a strengthening in real wages.

6. What Is the Outlook for Each Asset Class?

CASH AND DEFENSIVE ASSETS

Cash yields remain attractive but are likely to decline as Fed funds cuts continue. Municipal and corporate bond yields are similarly offering less forward return potential after very strong returns in 2025. Inflation continues to improve as shelter costs decline; moderating wage growth and AI related productivity gains help offset tariff related cost pressures on food and goods. If these trends persist, inflation should continue to move closer to the Federal Reserve’s target, reinforcing the case for lower policy rates and enhancing the appeal of longer-duration assets.

The appointment of a new Fed Chair this coming May introduces an additional layer of uncertainty. If markets perceive a shift toward less credible inflation management or greater political influence on monetary policy, longer-term inflation expectations could rise, pressuring the long end of the yield curve. We favor a measured approach to investing in interest rate sensitive bonds, balancing the attractive fundamentals against policy-related risks.

CREDIT ASSETS

Current yields for high yield corporate credit are still reasonably attractive, but less so than a year ago as both interest rates and credit spreads (the difference between Treasury yields and lower-quality, more credit-sensitive fixed income) decline. More appealing now are investments in business development corporations, or BDCs, which invest in floating-rate middle market private company debt. Robust underwriting standards at the highest quality BDCs and modest overall default rates and losses make certain BDCs appealing at current prices.

DIVERSIFIED MARKET STRATEGIES

Diversified Market Strategies are intended to provide a return stream that has a low correlation to both equity and bond markets and maintains a positive real (inflation-adjusted) expected return through a full market cycle. We believe there is a reasonable chance that geopolitical uncertainty remains elevated for the foreseeable future, making a small investment in gold and, for clients with the right risk profile, an even smaller investment in Bitcoin, a prudent portfolio allocation. Gold is a store of value, increasing by the rate of inflation or better over millenniums. Bitcoin has not been, due to its still high volatility, but it has similar properties in that it is widely accepted (at least relative to other digital assets) and its supply is structurally limited, leading to positive returns over all rolling three-year periods in its brief (17 year) history.

GROWTH ASSETS

After notching double digit growth in 2025, we expect earnings for the S&P 500 index to remain healthy in 2026. The largest U.S. technology companies’ earnings are likely to continue to outstrip the other 490 or so, but the gap is narrowing as increasing productivity fuels the broader market. Big Tech earnings are also being held back by massive capex spending. While we expect revenues and profits from AI-related spending to increase at these companies in the coming years, the return on investment must clear high hurdles to meet current investor expectations.

International earnings growth, while accelerating modestly, still meaningfully lags U.S. earnings. Again, while we remain underweight, where appropriate, we have been increasing allocations to international stocks in client portfolios throughout the past year for a few reasons: diversification away from mega-technology stocks; lower valuations (even after a run up last year, valuations internationally remain discounted (MSCI ACWI ex-US Forward PE ratio is 14.9x3); and near-term catalysts, including more fiscal spending in Europe and continued corporate governance reforms in Japan.

Finding the right balance between Big Tech stocks and a broadly diversified portfolio is the right path in our view. We aren’t shying away from the best of what Big Tech has to offer, but we are also intent on finding opportunities in more attractively valued stocks in sectors outside of technology, in smaller capitalization sectors and international markets.

PRIVATE MARKETS

Recent expanding private equity deal activity and less fundraising (meaning not as much capital available to chase those deals) creates a potentially attractive investment environment. Programmatic investment, with diversification across funds, investment style and vintage year, seems to us the best approach to this asset class. In private equity, we are currently focused on buyout and growth opportunities, investing with managers able to add operational value and generate attractive long-term return streams that can enhance risk-adjusted returns in portfolios with a reasonably long-time horizon.

Private credit managed by funds continues to take market share from banks and other regulated buyers, a trend that we expect to continue as banks both consolidate and derisk their balance sheets. We favor a combination of funds that loan money to private middle market companies and strategies that invest in asset-backed loans which provide a relatively higher degree of credit quality and add to portfolio income and diversification.

CONCLUSION

Strong economic and corporate fundamentals co-exist today with rich U.S. equity valuations and a concentrated market, leaving less margin for error. This could lead to both more volatility and lower returns in 2026 and perhaps for years to come. A disciplined, diversified approach remains the best defense against volatility and uncertainty. We remain focused on building robust client portfolios able to withstand a range of economic and market conditions, in the context of each client’s long-term financial goals.