John is the Chief Investment Officer of Evercore Wealth Management, responsible for the firm’s market outlook and asset allocation policy. He has over 30 years of experience managing balanced investment portfolios for high net worth clients and foundations and endowments.

Prior to joining Evercore in 2008, John was a managing director of U.S. Trust, which he joined in 1984. He was responsible for managing $2 billion of client assets, representing many of U.S. Trust’s most significant clients. Additionally, John served as the Chief Investment Officer of U.S. Trust of New York from 2003 to 2005, and as the head of Equity Investments and the Chair of the Equity Investment Committee from 2005 to 2008. For 15 years, he was an active participant in the formulation of overall investment strategy and a member of the U.S. Trust Investment Strategy Committee.

Prior to attending business school, John was on the staff of the U.S. Senate Labor and Human Resources Committee and worked on federal budget matters.

John received his B.A. from Bucknell University and an M.B.A. from New York University. He holds the Chartered Financial Analyst designation and is a former member of the Board of the New York Society of Security Analysts.

Adaptable, Dominant, Expensive: The Magnificent Seven

The S&P 500 has become so highly concentrated that it is taking on the higher risk and higher expected return characteristics of an insufficiently diversified portfolio. The largest market cap stocks in the S&P 500, appropriately dubbed the Magnificent Seven, now comprise almost 32% of the index and are growing faster than the remainder.

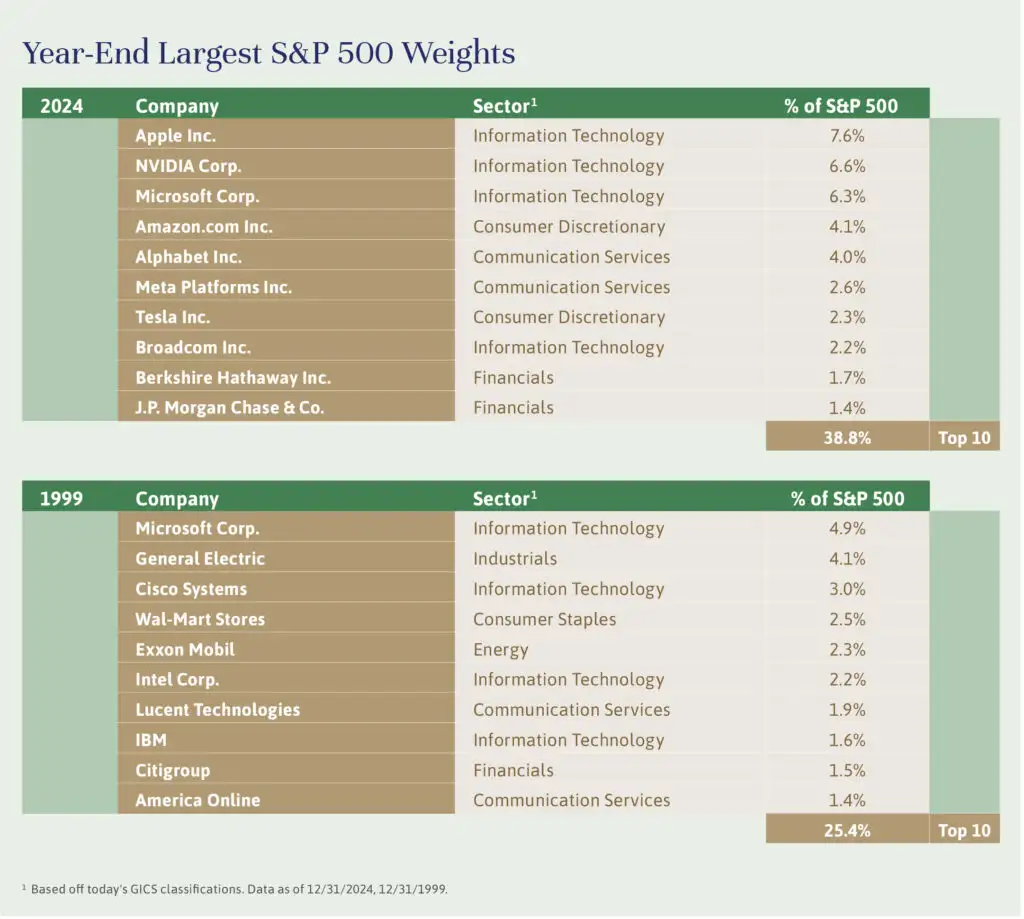

Prior periods of concentration involved large companies from very different industries, mostly blue-chip companies with strong balance sheets that had grown rapidly in the past but had evolved into risk-averse, conservatively managed companies. Take a look at the chart below, comparing this market with that of 25 years ago. The dominance of the leading companies is greater and less diverse.

The Magnificent Seven companies – Alphabet (Google), Apple, Amazon, Meta (Facebook), Microsoft, NVIDIA and Tesla – are among the most profitable, value-creating business entities ever devised. But they are all digital technology companies that are in large part betting their futures on the emerging AI technology.1 These companies not only have to capitalize on AI to meet current investor expectations, but they must do so soon.

It may take longer than investors currently expect, however. The promise of the internet back in 2000 was eventually realized, but it took years longer than companies and investors expected. Some companies never recovered. Others, like Microsoft, took over a decade to return to their old highs. Digital technology often creates a winner-takes-all dynamic; a global network effect and economies of scale whereby more users drive exponentially more usefulness and value. The main risk to an incumbent is a completely new technological innovation that changes the basic rules of the game. The recent launch of DeepSeek out of China is potentially just such an example.

It is unclear what proportion of these companies’ investment in AI is being spent on beating the other guy, rather than as the result of sober assessments of the potential returns. The Magnificent Seven are also running into the real-world constraint of electrical power capacity. The hyper-scaled data centers that Microsoft, Amazon, Alphabet and Meta are building with NVIDIA computer systems require more power than the current power grid can support, as we will discuss in the next issue of Independent Thinking.

Regulation is another pressing concern. These companies now dominate their respective spaces to the point that they could be considered near monopolies. Meta’s 77% share of social media, Google’s 80+% share of online advertising, and NVIDIA’s control of the latest AI chips are particularly striking.2 They can fend off competitors and earn unusually high margins – for now, that is. In his article, Adapting to Change: The Evolution of the Technology Market, Brian Pollak reviews government efforts to regulate or break up past monopolies and the risks now facing companies that could be considered the same.

It should also be noted that near monopolies are evident in other industries as well. Visa and Mastercard have a near duopoly in payment processing; Walmart, Costco and Home Depot continue to take market share from smaller competitors; and JP Morgan continues to pull away from its smaller rivals.

At the same time, there are at least two important emerging trends that could help smaller companies to grow faster. High interest rates, and day-to-day regulation fall far more heavily on smaller businesses. The Federal Reserve is in the process of lowering interest rates, and the new presidential administration should reduce regulation, even as it takes a closer look at Big Tech. It seems to us that a broadening out of stock market performance would be a healthy development, encouraging emerging innovation and competition.

In the interim, we believe we have positioned our portfolios to continue to benefit from the extraordinary performance of mega-cap stocks and better performance from the rest of the market. We are looking at new technologies earlier and considering the potential implementors. By retaining exposure to most of the Magnificent Seven but underweighting the group, we hope to mitigate concentration risks and to preserve and grow wealth.

1 Total projected CapEx and R&D spending by Alphabet, Apple, Amazon, Meta, Microsoft, NVIDIA and Tesla in 2025. FactSet, Company Data.

2 Source: Statista

This Independent Thinking® issue explores the challenges and opportunities of managing investment portfolios amid buoyant but increasingly volatile markets. It discusses the risks of market peaks, the potential for inflation