The U.S. economy appeared strong at the start of 2026, with robust – and broadening – corporate earnings and resilient labor markets. The next three months were interesting.

The rapid evolution of artificial intelligence, the emerging stresses in parts of the private credit market, and now war in the Middle East were – and still are – a lot for investors to process. Economists surveyed by Bloomberg in March rated the chances of recession at 30%, up slightly from 25% estimated in the February survey. But the recent market volatility so far reflects a repricing of risk rather than a deterioration in core economic conditions. If we do avoid recession, as seems likely, we believe that the probability of a bear market (a greater than 20% decline in equities), remains low. A decline in that ballpark would, we believe, represent a significant buying opportunity.

Let’s look at the risks individually and then consider their potential impact.

ARTIFICIAL INTELLIGENCE

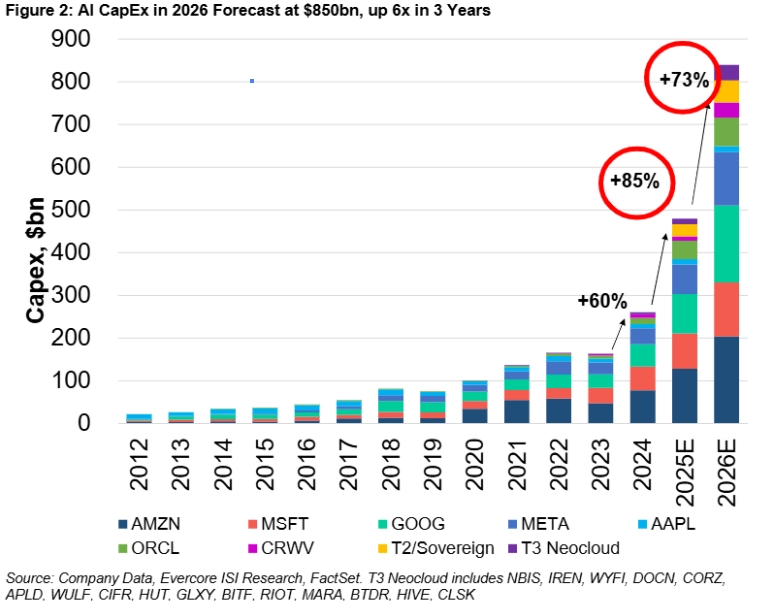

AI remains the most powerful force shaping the investing landscape. Capital expenditures tied to AI, which by some estimates could exceed $800 billion in 2026 (see chart from Evercore ISI below), continue to expand at an extraordinary pace, with significant investment in data centers, semiconductors, and supporting infrastructure. While some of this capital may not produce the returns sought by investors, it does not presently appear to have the characteristics of a bubble, as this spending has already become a meaningful contributor to economic growth and corporate earnings.

AGENTIC AI CREATING DIFFERENT COMPUTE DEMAND MODEL

At the same time, the pace of technological change is introducing a new layer of uncertainty. Investors are beginning to grapple with two longer-term questions.

First, will business models as we know them be disrupted? Software companies were in the market crosshairs in the first quarter, on investor predictions that much of the sector could be disintermediated by AI. This concern led to a sharp repricing – the S&P Software Index plunged around 25% in the quarter. But earnings expectations among more established software companies, such as Microsoft and Adobe, continue to rise.

Second, there is concern that labor will be displaced by AI. While still in early stages, AI has the potential over time to meaningfully alter labor demand, particularly in knowledge-based industries. We are likely to see new and very large, AI-focused companies enter the public markets. SpaceX, the owner of X.AI, has already entered the fray with its April 1 IPO announcement; others could include OpenAI and Anthropic.

While the current repricing reflects legitimate risks, it is also likely creating opportunities, particularly in companies with durable competitive advantages, strong balance sheets, and clear paths to monetization in an AI-driven environment.

PRIVATE CREDIT

The second area of concern is emerging stress within segments of the private credit market. Defaults and other indicators – such as payment-in-kind and non-accrual rates – are rising, albeit modestly from low levels. The most visible pressure is concentrated among leveraged software borrowers, where business models may be vulnerable to AI-driven disruption.

The more immediate issue is liquidity. The private credit market has grown significantly over the past decade, in part through retail-oriented fund structures offering periodic liquidity. In some cases, investor redemption requests have exceeded the natural liquidity of the underlying loans, resulting in gating. (Non-traded BDCs often limit the amount of money investors can redeem at once, usually to around 5% of total fund assets in a quarter. When investors try to redeem more than 5%, they can be subject to fund level gating, meaning they only receive a portion of the capital they are attempting to redeem.)

However, as our colleague Glenn Schorr of Evercore ISI notes, only about $200 billion of the more than $2 trillion in private credit assets, resides in the direct lending, non-traded BDC structures that are most susceptible to this type of redemption pressure.

We believe the risk is manageable rather than systemic. Underwriting standards have generally been stronger and leverage levels lower than in prior cycles, and direct exposure within the banking system is limited, reducing contagion risk. This environment is likely to drive greater dispersion in outcomes, with weaker managers and more concentrated strategies underperforming, while higher-quality lenders with disciplined underwriting, and better matching between fund assets and liabilities, can continue to generate attractive risk-adjusted returns.

GEOPOLITICS

The most immediate and visible risk in the quarter was the onset of war with Iran. Prices of liquid fuels, fertilizer, aluminum, helium, among other commodities are already materially higher, and are likely to pressure the already strained lower-end global consumer. If sustained, it could weigh on global growth. Still, as we have noted in prior communications, markets tend to differentiate between headline risk and durable changes to earnings and growth trajectories. This would require the current conflict to escalate, as opposed to stabilizing, de-escalating, or ending in the nearer term. At present, markets appear to be balancing these possibilities.

Bigger picture, the United States remains in a long-term economic battle with China with the highest stakes being the competition in and around AI. If one or the other wins the race to create ultra-powerful AI, the economic and geopolitical consequences could be far reaching. And while we believe a military conflict between the two superpowers over Taiwan remains unlikely, the broader economic competition could result in a higher propensity for hot wars involving economic partners of the two powers, sustainably raising uncertainty related to geopolitics.

Given this uncertain backdrop, we assess our views by asset class below.

CASH AND DEFENSIVE ASSETS

The Federal Reserve has paused rate moves for the time being as its members assess the balanced risks of inflation remaining above target (and potentially going higher due to energy price increases) and a subdued labor market. The expected new Fed Chair, Kevin Warsh, had previously indicated a predilection to cut rates when he takes over later this year, although he will need both consensus of the voting members and economic data backing. The market is currently not expecting any rate cuts for 2026, suggesting that cash yields, around 3.5% currently, should remain relatively stable for the balance of the year. Longer-term fixed income yields have risen since the start of the war, in both municipals and Treasuries, leaving most bond indices modestly negative for the quarter, and setting them up for more attractive returns for the balance of the year if rates stabilize.

CREDIT ASSETS

Credit spreads (the difference between risk-free Treasury yields and the yield of riskier bonds) widened for high yield corporate and securitized credit in the first quarter (from a very low ~2.7% as of the end of 2025 to a more average level of ~3.3% as of March 31, 2026 for the Bloomberg Corporate High Yield Index). But the change is not as large as expected relative to the negative headlines surrounding software disintermediation, the war and private credit. Much of this is because credit fundamentals, including health of corporate balance sheets, earnings growth and still low default rates, remain strong. In addition, the problems in the private credit markets are less prevalent in public credit – software sector exposure is in aggregate smaller within public credit markets and there are no fund liquidity or redemption concerns. Public BDCs meanwhile, which hold private direct loans, have seen more significant price deterioration in the quarter, with assets trading at a meaningful discount to net asset value, even for companies viewed to have strong underwriting and management teams. While these investments are likely to experience further volatility, as long-term investors, we believe they represent attractive value propositions today.

DIVERSIFIED MARKET STRATEGIES

Our Diversified Market Strategies asset class is intended to provide a return stream that has a low correlation to both equity and bond markets while maintaining a positive inflation-adjusted expected return through a full market cycle. We believe there is a reasonable chance that geopolitical uncertainty remains elevated, making a small investment in gold and, for clients with the right risk profile, an even smaller investment in Bitcoin, a prudent portfolio allocation. While gold has traded atypically since the U.S. and Israel attacked Iran, the reasons – including investors cashing in gains and the new focus on oil – appear temporary. We continue to believe a modest gold position has a place in a balanced portfolio allocation.

GROWTH ASSETS

The S&P 500 Index increased by less than 1% in between January 1, 2026, and the start of the Iran war on February 28, considerably lagging international markets and U.S. small cap indices. It then outperformed, as investors fled to the perceived safety of the U.S. dollar and the U.S energy independence. The S&P ended the quarter down around 4%, while international markets and U.S. small cap indices returned ~-1% and 1% respectively.

So far, the rise in uncertainty has impacted prices, not earnings expectations, leading to a modest decline in valuation – from over 22x forward earnings on the S&P 500 to around 20x. Full year earnings growth expectations for the S&P 500 remain high. Q1 earnings reports kick off this week and expectations continue to rise – to ~13% according to LSEG Datastream, and revenue growth is also expected to grow in the high single digits for the full year. International earnings and revenue growth are projected to be close to U.S. markets, while still selling at a meaningfully discounted PE ratio of around 14x. We remain overweight the U.S. market but continue to increase our international allocations.

PRIVATE MARKETS

Private equity markets have avoided some of the recent negative headlines experienced by their private credit brethren, but some of the same risks apply, notably exposure to software and questions around some of the mark-to-market and valuation methodologies. In addition, private equity distributions have experienced a multi-year lull, causing some institutional investors to shy away from new capital commitment. But with the fundraising markets more difficult, there is likely to be less capital to pursue new private equity deals, perhaps a positive for fresh private capital.

CONCLUSION

Uncertainty reinforces the need not just for portfolio diversification, but for resilience. A resilient portfolio is one that can endure a wide range of economic and market outcomes while remaining positioned to capture long-term opportunities. This requires adequate liquidity, with sufficient cash equivalents to meet near-term spending needs and prudent use of leverage, both within portfolios and at the company level, to avoid forced selling during periods of market stress. Periods of heightened uncertainty have historically created attractive opportunities for patient, disciplined investors. While we expect continued volatility in the near term, the underlying strength of the U.S. economy, ongoing innovation, and continued growth and improving breadth in corporate earnings all provide a solid foundation for long-term returns.